Riyadh Islamabad Forge New Investment Decade Through Reform Alignment

For much of the modern history of relations between Pakistan and Saudi Arabia, the balance sheet was political before it was economic. Security ties, labour migration, remittances, diplomatic solidarity and periodic financial assistance formed the grammar of a durable partnership. Yet the strategic environment of the mid 2020s is changing the language of that relationship. Saudi Arabia is redesigning itself through Vision 2030, a state led attempt to reduce hydrocarbon dependence, create new industries, deepen sovereign investment capacity and project commercial influence beyond the Gulf. Pakistan, after repeated cycles of debt distress, inflation shocks and reform reversals, is searching for a route to growth that is based less on consumption and emergency financing and more on investment, exports and productivity. If these two transitions are aligned with discipline, the coming decade could become the most economically consequential phase in Pakistan Saudi relations.

The attraction is obvious. Saudi Arabia has capital, strategic ambition and a growing appetite for overseas opportunities that can deliver both returns and geopolitical leverage. Pakistan has population scale, geostrategic geography, resource potential and underused sectors that require patient capital. Each country possesses what the other lacks. The problem has never been absence of complementarity. It has been absence of execution. Too many bilateral announcements have been rich in ceremony and poor in closure. The next decade will depend less on memorandums of understanding and more on contracts, permits, dispute resolution and measurable outputs.

Vision 2030 has already altered the behaviour of the Saudi state. Riyadh no longer thinks only as an oil exporter or regional power. It increasingly thinks as an investor, logistics planner, tourism developer and technology buyer. Its sovereign institutions seek assets across continents. Its industrial policy aims to create supply chains in mining, manufacturing, renewables, food security and services. This outward orientation changes how Saudi Arabia sees partners. Countries that once mattered mainly for diplomatic alignment now matter for economic utility. Pakistan therefore has an opening, but only if it can present itself as investable rather than merely friendly.

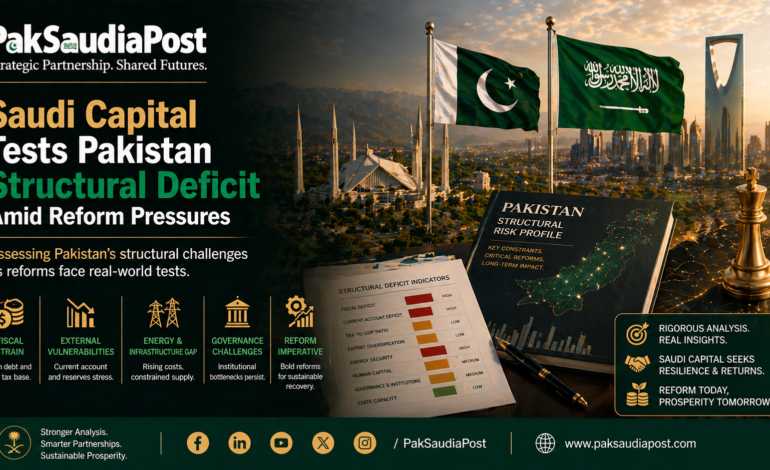

Pakistan’s own reform debate has slowly matured under fiscal pressure. Successive balance of payments crises have made one fact unavoidable. Consumption funded by imports and debt cannot sustain a nation of nearly a quarter billion people. The country needs foreign direct investment, export diversification, tax broadening, energy rationalisation and governance reform. Those words have been repeated for years, but crisis has given them sharper urgency. If policymakers can convert necessity into policy continuity, Pakistan may finally become a location where long term Gulf capital is willing to stay.

Mining offers the clearest test case. Pakistan possesses significant untapped mineral wealth, most notably in Balochistan. Copper and gold reserves at Reko Diq have become symbols of what the country might achieve if resource nationalism is replaced by competent resource management. Saudi investors, looking to secure exposure to strategic minerals essential for industrial diversification and global energy transition technologies, have understandable interest in such assets. For Pakistan, successful Saudi participation would do more than bring capital. It would signal that high level investors believe contracts can be honoured and operations protected. That reputational effect may be worth almost as much as the money itself.

Yet mining also reveals the risks. Pakistan has a history of legal disputes, centre province tensions and policy reversals in extractive sectors. Foreign investors do not fear risk alone. They fear arbitrary risk. If permits are delayed, royalties contested or courts inconsistent, enthusiasm will cool quickly. Riyadh can tolerate commercial uncertainty, but not administrative chaos. Thus the true mine to be developed may be institutional trust.

Logistics is another arena where alignment is plausible. Saudi Arabia seeks to become a global transport and trade hub connecting Asia, Africa and Europe. Pakistan sits at the intersection of South Asia, the Gulf, Central Asia and western China. Ports, dry ports, warehousing corridors, cold chains and freight digitisation could convert Pakistan from a transit aspiration into a functioning node. Gwadar attracts headlines, but the broader opportunity is national. Karachi’s maritime scale, road and rail modernisation, border trade formalisation and air cargo expansion could all benefit from Gulf capital and management expertise.

The challenge here is that infrastructure without systems creates monuments, not commerce. Pakistan has often invested in concrete more successfully than in governance. Customs reform, predictable tariffs, digital documentation and anti-smuggling enforcement matter as much as highways. Saudi capital can help build assets, but only Pakistani state capacity can make them productive.

Tourism may appear secondary compared with minerals or ports, yet it carries strategic value. Saudi Arabia is building a major tourism industry at home and accumulating experience in hospitality, destination branding and event management. Pakistan has extraordinary but underdeveloped assets in mountain tourism, heritage circuits, religious tourism and eco destinations. Joint ventures in hotels, aviation services, training institutes and digital booking ecosystems could create employment intensive growth. Tourism also changes narratives. A country known only through security headlines becomes visible through landscapes, culture and services.

Still, tourism depends on mundane basics. Clean cities, reliable transport, visa efficiency, policing standards and environmental management are more decisive than slogans. Pakistan has long advertised potential while underinvesting in visitor experience. If Saudi partners enter this field, they will demand standards that could usefully discipline domestic institutions.

Food security is perhaps the most structurally compelling domain. Saudi Arabia’s climate and water constraints ensure continued dependence on imported food. Pakistan has agricultural scale, diverse climates and labour depth. Rice, livestock, processed foods, fruits and halal branded products could anchor a bilateral food corridor. Saudi investment in storage, irrigation technology, seed systems, refrigerated logistics and quality certification would raise yields while securing supply.

Yet agriculture is politically sensitive. Land rights, provincial authority, water allocation and farmer interests complicate large projects. Pakistan must avoid simplistic narratives of selling land to foreigners while also resisting reflexive protectionism that blocks productive partnerships. The better model is joint value chains that improve domestic productivity and export capacity rather than enclave farming schemes that provoke backlash.

Renewable energy may become the most future oriented sector of all. Saudi Arabia wants leadership in new energy systems, while Pakistan suffers from expensive imported fuels, circular debt and chronic power distortions. Solar parks, wind corridors, battery assembly, grid management technologies and green hydrogen pilots could align Saudi capital with Pakistani necessity. Because Pakistan enjoys strong solar irradiation and significant wind zones, the economics are increasingly persuasive.

But energy reform is notoriously political. Tariffs, subsidies, transmission losses and payment arrears can erode even well designed projects. Investors need confidence that generated electricity will be purchased and paid for. Pakistan cannot invite strategic capital into a financially broken power market without first repairing incentives.

Media narratives around this relationship are evolving. In earlier decades, Pakistani discourse often portrayed Saudi Arabia as a benevolent rescuer providing deposits, oil facilities or employment opportunities. That sentiment has not vanished, but it is now contested by a younger and more commercially minded audience. On business channels, digital platforms and policy forums, the preferred language is shifting from aid to investment, from charity to partnership, from patronage to returns. This matters because public narratives shape political space. Governments find it easier to pursue reforms when citizens expect productivity rather than gifts.

Saudi media too has changed tone. Pakistan is less often discussed only as a brotherly ally and more frequently as a market, workforce partner and strategic geography. This reflects Riyadh’s own transformation. A state trying to attract tourists, list companies and deploy sovereign capital naturally adopts a more transactional worldview. That should not be mistaken for diminished friendship. It is friendship adjusted to economics.

There are, however, reasons for caution. Pakistan’s record with foreign investors remains mixed. Tax disputes, sudden regulatory shifts, energy bottlenecks and foreign exchange controls have all damaged credibility. Even when central governments are supportive, implementation can stall in provincial offices or courts. Investors remember not speeches but delays. Unless Islamabad creates an empowered one window system with real authority, bilateral ambitions may again drown in bureaucracy.

Macroeconomic stability is equally essential. No investor wants to enter a market where currency crises recur every few years. IMF programmes, though politically difficult, can provide discipline and signalling value if paired with domestic ownership of reform. Saudi capital is more likely to arrive at scale when it complements stabilisation rather than substitutes for it. Deposits can buy time. They cannot buy competitiveness.

Pakistan must also manage the optics of balancing external relationships. China remains a major infrastructure partner through the China Pakistan Economic Corridor. The United Arab Emirates has commercial interests. Western institutions influence finance. Saudi investment need not displace any of these ties. Indeed, a mature strategy would welcome multiple partners across sectors. But coherence matters. Competing promises to different capitals can create confusion. Islamabad should articulate a clear investment map showing where each partner fits.

For Saudi Arabia, Pakistan is attractive but not unique. Riyadh has opportunities from Africa to Southeast Asia to Europe. Capital is mobile and comparative. If Pakistan assumes sentiment guarantees priority, it will be disappointed. Saudi decision makers increasingly evaluate projects through returns, governance quality and strategic fit. That professionalisation should be welcomed in Islamabad, because it rewards reformers.

The labour dimension remains important. Millions of Pakistanis have worked in the Gulf, sending remittances that supported families and national reserves. As Saudi Arabia upgrades its economy, demand for higher skilled labour will rise while low skill roles may narrow. Pakistan should therefore align vocational training, language skills and technical certification with Saudi labour market needs. Human capital mobility can complement capital mobility.

The ideal bilateral compact would combine five tracks. First, anchor investments in mining, energy and logistics. Second, a food security partnership based on technology and exports. Third, skills pipelines for Saudi labour demand. Fourth, financial cooperation including Islamic finance and project funding. Fifth, institutional mechanisms that solve disputes quickly and monitor progress publicly. Such architecture would move the relationship beyond episodic diplomacy into durable economics.

What would success look like by 2035. Pakistan would have several operating Saudi backed industrial and resource projects, rising non debt capital inflows, improved export capacity and thousands of skilled jobs. Saudi Arabia would gain profitable assets, secure supply chains, strategic access and a large partner market. The relationship would be measured less by emergency deposits announced during crises and more by earnings reports, cargo volumes and production data.

What would failure look like. Grand summits would continue. Delegations would exchange promises. Headlines would celebrate billions pledged. Months later, little would move beyond committees. Pakistan would return to borrowing cycles. Saudi Arabia would redirect capital elsewhere. Familiar warmth would survive, but opportunity would not.

History gives both countries reason to be ambitious and reason to be sceptical. They have deep political trust, people to people ties and longstanding strategic habits. Those are valuable assets. But they are no substitute for institutions. The next decade can become transformative only if both sides accept a modern truth. In the age of competitive capital, friendship opens doors, but reform closes deals.

A Public Service Message