Saudi Capital Tests Pakistan Structural Deficit Amid Reform Pressures

Pakistan’s economic debate often swings between panic and hope. In moments of crisis, the country looks outward for emergency liquidity. In moments of calm, it promises structural reform. The distance between those two moments has historically been short. Few relationships illustrate this pattern more clearly than Pakistan’s ties with Saudi Arabia. For decades, Riyadh has served as a trusted source of diplomatic backing, labour market opportunity, oil facilities and occasional financial support when reserves thinned and markets turned anxious. Yet the central question of the present decade is different. Can Saudi capital do more than stabilise Pakistan in distress. Can it help cure the chronic investment deficit that keeps the economy trapped in low productivity, shallow exports and repeated dependence on external rescue.

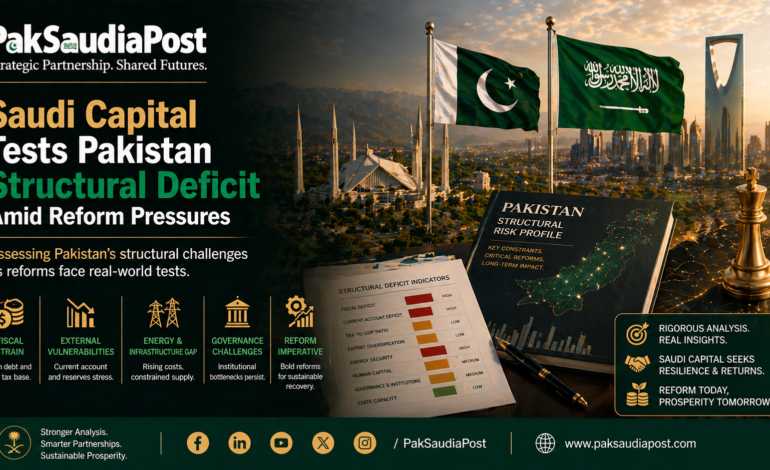

This question matters because Pakistan’s problem is not merely cyclical. It is structural. The country saves too little, invests too little, exports too narrowly and taxes too weakly. Domestic private investment has long been constrained by policy uncertainty, high borrowing costs, energy distortions and governance friction. Public investment, meanwhile, has been crowded out by debt servicing, security expenditure and recurrent fiscal pressures. The result is an economy capable of bursts of consumption but less capable of sustained transformation. Without a durable rise in investment, growth repeatedly runs into balance of payments limits.

Saudi Arabia enters this picture at a moment of its own transformation. Under Vision 2030, Riyadh is repositioning itself from a hydrocarbon dependent rentier state into a diversified investment power. The kingdom’s sovereign institutions, especially the Public Investment Fund, have become global actors seeking returns, strategic assets and new sectors. Saudi firms are increasingly outward looking. Their calculus is commercial as much as political. This creates opportunity for Pakistan, but only if Islamabad understands that modern Saudi capital behaves differently from older Saudi assistance. It asks harder questions, demands clearer rules and expects measurable outcomes.

For Pakistan, the attraction of Saudi investment is immediate. Unlike short term debt flows or volatile portfolio money, strategic foreign direct investment can create factories, mines, logistics platforms and energy assets. It can transfer technology, improve management practices and generate employment. It can also provide a signalling effect. If sophisticated Gulf investors commit substantial funds, others may interpret that as confidence in Pakistan’s direction. In markets where sentiment can be decisive, one credible investor often attracts another.

Yet it is important to distinguish between three forms of Saudi engagement. The first is financial support such as deposits that help foreign exchange reserves. The second is concessional facilities such as deferred oil payments that ease near term pressure. The third is productive investment that expands future capacity. Pakistan has historically received more of the first two than the third. The challenge of this decade is to reverse that ratio.

Consider refining and energy. Pakistan imports significant petroleum products and has long discussed upgrading refining capacity. Saudi participation in large downstream energy projects could reduce inefficiencies, improve standards and create industrial linkages in petrochemicals. Such investment would be more valuable than another temporary reserve injection because it addresses recurring external vulnerabilities. Every barrel processed more efficiently at home strengthens resilience. But energy projects are complex. They require land acquisition clarity, pricing frameworks, environmental permissions and confidence that policy will not be rewritten after capital is sunk.

Mining offers another promising frontier. Pakistan’s untapped copper, gold and mineral resources are globally relevant at a time when strategic metals are increasingly prized. Saudi Arabia itself is developing a mining strategy and understands the value chain. Joint ventures in Pakistan could serve Saudi industrial diversification while monetising dormant Pakistani assets. Yet the extractive sector magnifies governance flaws. If royalties are disputed, licences politicised or local communities excluded, investment can stall for years. Resource wealth without administrative competence becomes a curse of delay.

Agriculture and food security may be even more strategic. Saudi Arabia’s environmental constraints ensure continued dependence on imported food. Pakistan has scale in rice, livestock, fruits and halal products. Saudi capital in storage, cold chains, irrigation technology and processing facilities could turn Pakistan from a raw supplier into a higher value export partner. This would create rural employment and foreign exchange. Still, agriculture in Pakistan is entangled with water scarcity, fragmented landholding and provincial politics. Without domestic reform, even generous financing risks underperformance.

Then there is logistics. Pakistan’s geography is often described as an advantage, but geography alone earns nothing. Location must be converted into systems. Ports, roads, customs efficiency, warehousing and digital trade facilitation determine whether a country becomes a corridor or merely a map point. Saudi investors seeking regional connectivity may find Pakistan interesting, especially as Gulf trade patterns evolve. Yet if trucks queue for days, customs rules shift unpredictably and rail modernisation lags, strategic geography remains rhetorical.

The largest obstacle to Saudi investment is not lack of opportunity. It is credibility. Pakistan has a habit of announcing reforms faster than implementing them. Investors study precedent. They note tax disputes with foreign companies, currency controls during stress episodes, delayed payments in the power sector and abrupt regulatory changes. Political transitions can also unsettle commitments. When governments change frequently, counterparties wonder whether signatures endure. Saudi investors are familiar with frontier markets, but familiarity with risk does not equal tolerance for avoidable dysfunction.

This is where IMF programmes become relevant. In Pakistan’s domestic discourse, IMF conditionality is often treated as externally imposed pain. Yet from an investor perspective, an IMF framework can provide reassurance that macroeconomic discipline, however imperfect, is being restored. Fiscal consolidation, exchange rate realism and structural benchmarks are not sufficient for investment, but they can be necessary preconditions. Saudi capital is more likely to arrive at scale when macro chaos is contained. The kingdom does not wish to place long term money into an economy permanently firefighting short term imbalances.

At the same time, there is a paradox. If Pakistan relies on Saudi deposits to navigate IMF negotiations, and then postpones reforms once pressure eases, Saudi support unintentionally sustains the very cycle it seeks to relieve. Temporary relief can become moral hazard. The wiser Saudi approach would be to tie future assistance more explicitly to reform milestones and productive opportunities. In other words, capital should reward adjustment, not replace it.

Media narratives in Pakistan often exaggerate the immediacy of Gulf investment. Headlines celebrate billions discussed during high level visits. Social media converts expressions of interest into presumed cash inflows. Markets sometimes rally on announcements alone. But seasoned observers know that memorandums are not money. Between pledge and project lies feasibility studies, legal documentation, financing structure, regulatory approval and operational planning. Pakistan’s credibility suffers when public communication treats intent as execution. A more mature discourse would celebrate closures, not ceremonies.

Saudi media has evolved in its own way. Pakistan is increasingly framed not only as a brotherly nation but as a market with potential contingent on reform. This is a subtle but important shift. It reflects Riyadh’s own modernisation. A state learning to price assets and benchmark returns naturally applies commercial logic abroad. Pakistan should welcome that realism. Sentimental exceptionalism often excuses weak performance. Commercial scrutiny can sharpen reform incentives.

There is also competition. Saudi Arabia has many options for deploying capital. Egypt offers scale and proximity. The Gulf itself absorbs vast spending. Africa presents agricultural and mining opportunities. Southeast Asia offers manufacturing ecosystems. Europe and North America provide stable assets. Pakistan is competing in a global marketplace for attention. Historical friendship provides access, not entitlement. If Islamabad assumes that strategic nostalgia guarantees investment, it misreads the age.

What then would make Pakistan genuinely attractive. First, policy continuity. Investors can price taxes and tariffs if they are stable. They cannot price improvisation. Second, dispute resolution. Commercial conflicts should be settled quickly through trusted mechanisms. Third, foreign exchange confidence. Investors must be able to repatriate profits under clear rules. Fourth, infrastructure reliability, especially power and logistics. Fifth, administrative simplicity. One window investment agencies are common slogans; they become meaningful only when they override fragmented bureaucracy.

Pakistan also needs to think beyond mega projects. Large headline investments matter, but medium sized ventures often create broader employment and supply chain depth. Saudi participation in pharmaceuticals, packaging, food processing, data centres, tourism services and vocational institutes could prove as transformative as any flagship refinery. Diversified investment reduces political risk and distributes gains geographically.

The labour relationship remains central. Millions of Pakistanis work in Saudi Arabia, and remittances remain a vital stabiliser. But Saudi labour market reforms favour skills upgrading and localisation. Pakistan should therefore negotiate not only labour quotas but training pathways. If Pakistani workers move into healthcare, engineering, hospitality management and technical trades, remittance quality rises even if low skill volumes plateau. Human capital is itself an investment channel.

For Saudi Arabia, helping Pakistan close its investment deficit would deliver strategic returns. A more stable and prosperous Pakistan is a larger market, a more reliable security partner and a useful bridge to South Asia and beyond. It would also validate Riyadh’s image as a serious development investor rather than merely a provider of crisis cash. Success in Pakistan could become a model for selective Gulf capital diplomacy.

Still, neither side should romanticise the task. Structural deficits accumulated over decades are not rescued by one partner or one summit. They require domestic political bargains inside Pakistan: broader taxation, energy reform, export discipline, urban productivity and institutional competence. Foreign capital can accelerate progress, but it cannot substitute for governance. If local incentives remain distorted, external money will either demand very high returns or stay away.

The real test is whether both capitals can move from transactional reflexes to strategic patience. Pakistan must stop viewing Saudi Arabia chiefly as a source of emergency liquidity. Saudi Arabia must avoid treating Pakistan as a recurring rescue case. Instead, both should define a decade long agenda with annual benchmarks, sector priorities and transparent monitoring. That would replace episodic drama with cumulative progress.

Can Saudi capital rescue Pakistan’s structural investment deficit. Rescue is the wrong word. It suggests salvation from outside. Pakistan can only rescue itself through reform. But Saudi capital can catalyse that rescue if it enters productive sectors, rewards discipline and insists on credible execution. If used wisely, Riyadh’s money could become leverage for transformation. If used poorly, it will merely finance another intermission before the next crisis.

A Public Service Message