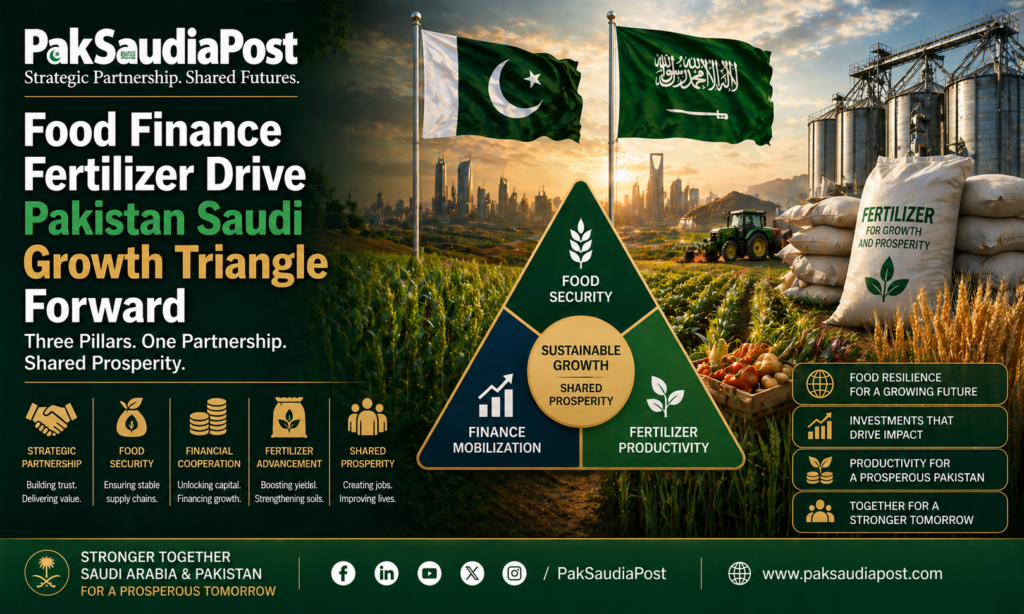

Food Finance Fertilizer Drive Pakistan Saudi Growth Triangle Forward

The old architecture of Pakistan Saudi economic relations rested on three pillars. Oil flowed eastward, labour flowed westward and money returned home as remittances or periodic financial support. That model created endurance, but not depth. It stabilised ties without fully modernising them. In the current decade, however, both states face pressures that demand a more sophisticated arrangement. Saudi Arabia seeks food security, diversified investments and financial influence beyond hydrocarbons. Pakistan seeks export expansion, industrial renewal and durable foreign exchange earnings. Out of these parallel needs, a new triangle is emerging. Food, fertilizer and finance are becoming the practical engines of a bilateral relationship once defined mainly by energy diplomacy and strategic sentiment.

This shift is neither accidental nor cosmetic. It is the result of structural changes in the global economy. Climate volatility has made food supply chains a strategic matter. The pandemic and later geopolitical disruptions revealed how quickly trade routes can fracture. Fertilizer markets have become sensitive to war, gas prices and sanctions. Finance is being reshaped by digital payments, Islamic banking expansion and new patterns of sovereign investment. Countries that once traded only goods now compete through systems. For Pakistan and Saudi Arabia, the opportunity lies in linking these systems intelligently.

Food security is perhaps the clearest case. Saudi Arabia’s domestic geography imposes obvious limits. Water scarcity, harsh climate and environmental sustainability concerns constrain large scale agricultural self sufficiency. Even wealthy states cannot manufacture rainfall. The kingdom therefore requires reliable external food sources, preferably diversified across partners and protected by long term contracts. Pakistan, by contrast, possesses river systems, varied climates, arable land and a large agricultural workforce. It produces rice, wheat, fruits, vegetables, livestock and fisheries products, though often below potential. In theory, this complementarity is ideal. Saudi demand meets Pakistani capacity.

Yet theory has often exceeded practice. Pakistan’s agriculture remains burdened by low yields, fragmented landholding, outdated seed usage, weak storage systems and costly post harvest losses. Farmers may produce, but supply chains frequently fail. Produce spoils before export. Cold chains are patchy. Quality certification can be inconsistent. Transport costs erode margins. A country that could feed others sometimes struggles to monetise its own abundance. This is where Saudi capital and management expertise could become catalytic. Investment in warehousing, refrigerated logistics, modern slaughterhouses, packaging plants and traceability systems would transform Pakistan from a commodity seller into a premium supplier.

Rice illustrates the point. Pakistan is already a notable exporter, especially in aromatic varieties. But much of the value chain remains underdeveloped. Branding, processing, retail packaging and stable long term procurement agreements could substantially raise returns. Saudi supermarkets and distributors seeking dependable halal certified products could anchor such demand. The same applies to meat and poultry. Pakistan has livestock potential, but export scaling requires disease control, processing standards and cold chain reliability. Saudi financing paired with Pakistani production could create an integrated halal protein corridor stretching from farm to Gulf consumer.

Fruits and vegetables offer another frontier. Pakistan’s mangoes, citrus, dates and other seasonal produce are admired but inconsistently positioned in premium markets. Better grading, packaging and air cargo systems could change that. Here, relatively modest investments may generate outsized results. Not every bilateral breakthrough requires a multibillion dollar refinery. Sometimes it requires a functioning refrigerated terminal and a digital procurement platform.

There are political sensitivities, of course. Any discussion of foreign involvement in agriculture can trigger anxieties about land ownership, sovereignty or elite capture. Pakistan should avoid crude models in which vast tracts are handed to outsiders under opaque terms. Such schemes generate suspicion and often disappoint commercially. The wiser route is joint ventures, contract farming, technology partnerships and processing investments that raise productivity while keeping domestic legitimacy intact. Saudi Arabia needs supply reliability more than territorial symbolism. Pakistan needs value creation more than headline acreage deals.

If food is the first side of the triangle, fertilizer is the second. Modern agriculture without nutrient security is aspiration without yield. Global fertilizer markets have become more volatile due to energy price swings and geopolitical shocks. Since many fertilizer products depend on natural gas or mineral inputs, disruptions can rapidly inflate farming costs. Pakistan has domestic fertilizer capacity but also recurring shortages, pricing distortions and uneven access. Saudi Arabia, with petrochemical strength and industrial scale, can play a significant role in stabilising supply and deepening cooperation.

Joint ventures in urea production, phosphate sourcing, blending plants and distribution systems could improve both affordability and efficiency. Beyond traditional fertilizer, cooperation could extend to precision agriculture products, soil analytics and water efficient nutrient delivery. Pakistan’s farming challenge is not simply lack of inputs. It is often misuse of inputs. Over application in some areas, under application in others and weak extension services reduce productivity and damage soil health. Saudi backed agritech platforms could modernise farm decisions through data rather than habit.

This matters strategically. Higher agricultural productivity lowers food inflation, raises export surplus and eases pressure on imports. In Pakistan, where inflation frequently destabilises politics, better fertilizer systems are not merely technical matters. They are instruments of macroeconomic stability.

The third side of the triangle is finance, and perhaps the most transformative over time. The bilateral economic relationship has long depended on remittances from Pakistani workers in Saudi Arabia. These flows remain vital, supporting households and strengthening reserves. But the financial relationship can become far broader. Islamic banking, cross border digital payments, diaspora investment products, sukuk markets, fintech partnerships and project finance all offer routes to deeper integration.

Saudi Arabia is positioning itself as a global centre of Islamic finance and investment. Pakistan has a large Muslim population, growing demand for Sharia compliant products and a need for long term capital. Greater banking integration could lower transaction costs, improve trade settlement and mobilise savings. Pakistani banks with Gulf partnerships could expand services for exporters and workers alike. Saudi institutions could support infrastructure financing through structured instruments rather than ad hoc state assistance.

Digital remittances are especially important. Millions of Pakistani workers still face fees, delays or informal channels when sending money home. Modern payment rails, mobile wallets and regulated fintech corridors could increase efficiency and transparency. Even small reductions in cost matter when multiplied across millions of transactions. A percentage saved in fees is income returned to households.

There is also scope for diaspora investment vehicles. Pakistani workers in Saudi Arabia have historically sent money for consumption, housing or family support. New instruments could channel part of these savings into productive uses such as SME funds, municipal bonds or export ventures. Trust will be crucial. Many overseas Pakistanis hesitate because of governance concerns. But properly structured and transparently managed vehicles could unlock a meaningful source of patient capital.

The labour market dimension cannot be ignored. Saudi Arabia’s own reforms are reshaping demand. As the kingdom builds tourism, logistics, healthcare, entertainment and advanced services, it will require different skills than in earlier eras. Low skill labour demand may not grow as before, while technical and professional roles expand. Pakistan must adapt vocational training accordingly. Language skills, hospitality standards, nursing qualifications, coding, engineering maintenance and industrial trades can all enhance worker competitiveness. The future of remittances may depend more on quality than quantity.

Media narratives around this evolving triangle are instructive. In Pakistan’s traditional discourse, Saudi economic relations were often reduced to oil generosity and brotherly assistance. Younger commentators increasingly reject that passive framing. On business media and digital platforms, the preferred language is entrepreneurship, supply chains and investment ecosystems. Aid is seen as temporary. Market access is seen as strategic. This shift reflects a broader generational impatience with dependency narratives.

Saudi media likewise portrays partnerships through the lens of Vision 2030 pragmatism. Countries are discussed less as symbolic allies and more as nodes in networks of food security, logistics and capital deployment. Pakistan can benefit from this perspective if it demonstrates seriousness. If not, Riyadh has alternatives from Africa to Central Asia. Sentiment remains valuable, but opportunity cost now matters more than before.

There are risks to the triangle. Pakistan’s policy inconsistency remains the largest. Export bans imposed during domestic shortages can damage reliability. Sudden tariff changes confuse investors. Bureaucratic delays weaken enthusiasm. Weak contract enforcement raises the cost of doing business. Saudi investors, like all investors, can tolerate normal commercial risk. They are less patient with preventable disorder.

Climate change poses another challenge. Pakistan’s floods, drought cycles and water stress threaten agricultural stability. Any long term food partnership must include resilience measures such as better irrigation, crop insurance, seed adaptation and storage systems. Saudi financing could support such adaptation, but domestic planning must lead. Food security built on vulnerable production is false security.

Geopolitics also intrudes. Red Sea disruptions, shipping insurance spikes or regional tensions can reshape freight economics. This makes diversified transport routes and inventory planning more important. It also strengthens the case for processing closer to source rather than shipping only raw produce. Value added exports are often more resilient than bulk commodities.

For Pakistan, the deeper lesson is strategic. It cannot continue to approach external partners primarily through fiscal desperation. When reserves fall, capitals call friendly capitals. That cycle has diminishing returns. Stronger states negotiate from opportunity, not emergency. By building a food, fertilizer and finance framework with Saudi Arabia, Pakistan can convert a historically reactive relationship into a proactive one.

For Saudi Arabia, the partnership offers more than supply contracts. A stable and growing Pakistan is a large market, a labour partner, a strategic geography and a political asset in the wider Muslim world. Supporting productive sectors rather than only balance sheet rescue aligns with Riyadh’s own transformation into an investment power.

What would success look like within a decade. Pakistani branded food products on Saudi shelves at scale. Modern cold chains linking farms to Gulf ports. Joint fertilizer ventures lowering input volatility. Digital remittance platforms reducing costs. Skilled Pakistani professionals moving into higher wage Saudi sectors. Bilateral trade financed increasingly through sophisticated Islamic instruments rather than state interventions.

What would failure look like. Repeated summit announcements, little implementation, sporadic aid packages, unchanged farm inefficiency and remittances carrying a relationship that should have matured long ago.

The emerging triangle is therefore more than an economic theme. It is a test of whether two longstanding partners can modernise their connection to fit a harsher and more competitive century. Food provides necessity. Fertilizer provides productivity. Finance provides scale. If joined intelligently, they could do what symbolism alone never could. They could make the Pakistan Saudi partnership commercially indispensable.

A Public Service Message